Gavi progress report 2024

A year of landmark accomplishments, historic progress on immunisation, significant challenges and change for Gavi and the world.

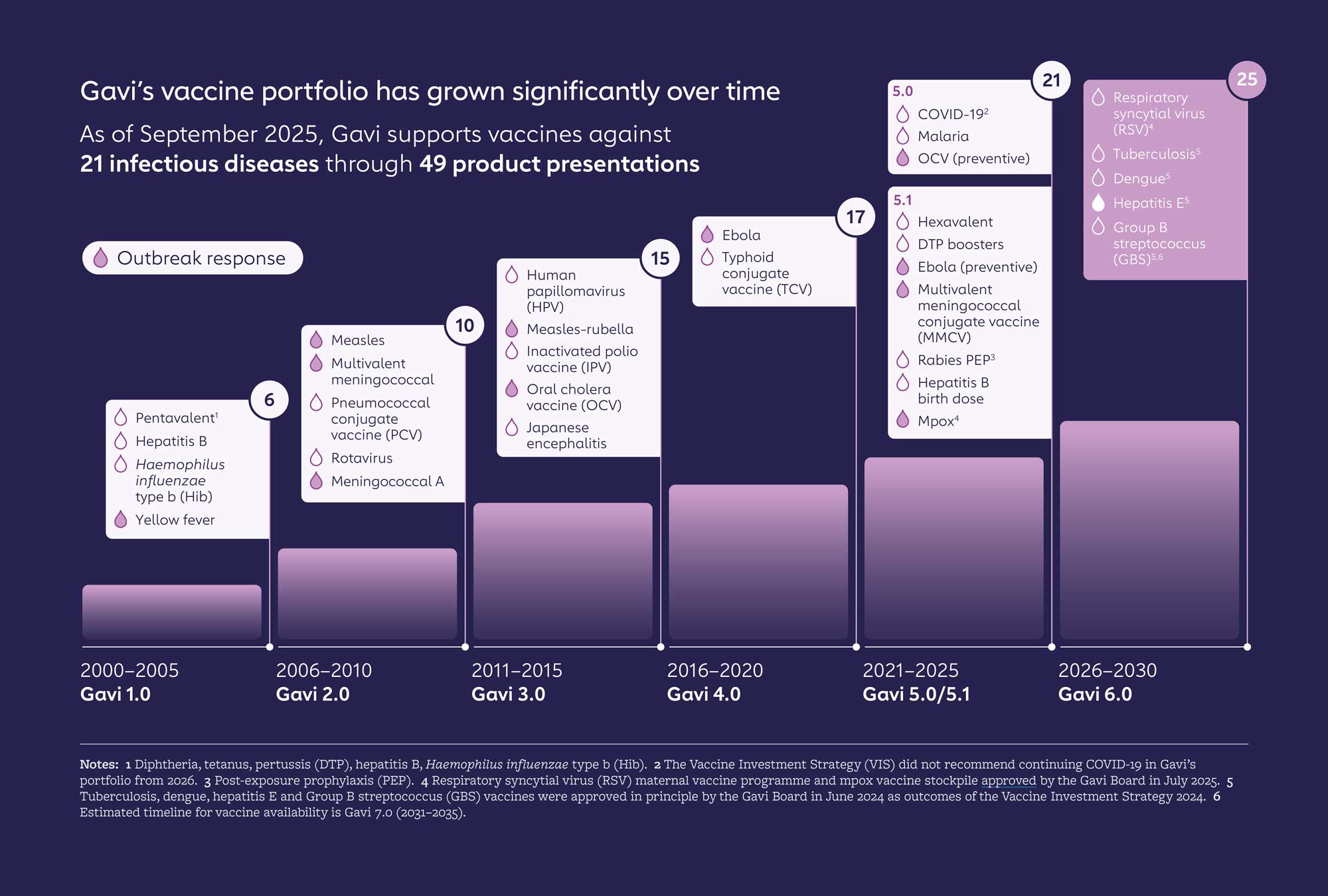

Welcome to Gavi’s 2024 Annual Progress Report, the fourth of Gavi’s 2021–2025 strategic period (Gavi 5.0/5.1). 2024 was a year of landmark accomplishments, historic progress on immunisation, significant challenges and change for Gavi and the world. It was a year in which the Vaccine Alliance demonstrated its resilience and laid the foundations for our coming five-year strategic period.

Mission indicators

Despite the confluence of risks that the world continued to face in 2024, Vaccine Alliance partners and countries are on track to achieve most of our six mission indicators for the 2021–2025 strategic period.

VaccinesWork 2024: our most read stories

Climate change causes malaria cases to triple in northwest Pakistan

In the wake of 2022’s floods, provincial health leaders say they need a new “climate-change specific” plan.

Zipline drones wing vaccines to malaria-prone western Kenya

From rabies post-exposure prophylactics to measles and malaria vaccines, drones are getting life-saving shots to kids in remote parts of Kisumu.

How Uganda’s immunisation programme helped reduce child mortality

In Uganda in 2011, 90 children out of every 1,000 live births died before their fifth birthday. Today, that figure has dropped to 52 – and health leaders say vaccination has been key to the change.

Strategic goals

The Vaccine Alliance’s mission is: to save lives and protect people’s health by increasing equitable and sustainable use of vaccines. This mission is supported by four strategic goals, each with its own set of strategy indicators. Learn more below.

The vaccine goal

Introduce and scale up vaccines

The equity goal

Strengthen health systems to increase equity in immunisation

The sustainability goal

Improve sustainability of immunisation programmes

The healthy markets goal

Ensure healthy markets for vaccines and related products

The vaccine goal:

Introduce and scale up vaccines

Routine immunisation in 2024: increasing breadth of protection

The WHO/UNICEF Estimates of National Immunization Coverage (WUENIC) released in July 2025 show progress towards several of Gavi’s strategic objectives in the penultimate year of the Gavi 5.0/5.1 strategy (2021–2025). Gavi-supported countries are protecting more children, against more diseases, than ever before in history – and coverage rates are steadily on the rise following declines during the COVID-19 pandemic.

Gavi-supported vaccine introductions and preventive campaigns took place in 2024 – in addition to 50 outbreak response vaccination campaigns supported by Gavi.

girls fully immunised against HPV with Gavi support in 2024 alone – more than the previous ten years combined.

countries accessed cholera, meningococcal and yellow fever vaccines through Gavi-supported emergency stockpiles a total of 44 times in 2024.

The 57 Gavi-supported countries increased breadth of protection with vaccines in the Gavi portfolio to 63%, up 8 percentage points from 2023.

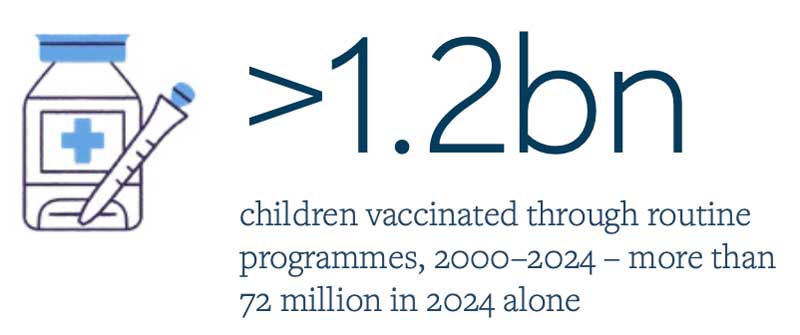

Since 2000, more than 1.2 billion children have been reached through routine immunisation with Gavi support – surpassing the Alliance goal to protect 1.1 billion children by 2025.

Vaccine focus: human papillomavirus (HPV) vaccine

Protects against the main causes of cervical cancer, which claimed the lives of around 350,000 women in 2023, of which over 90% are in low- and middle-income countries.

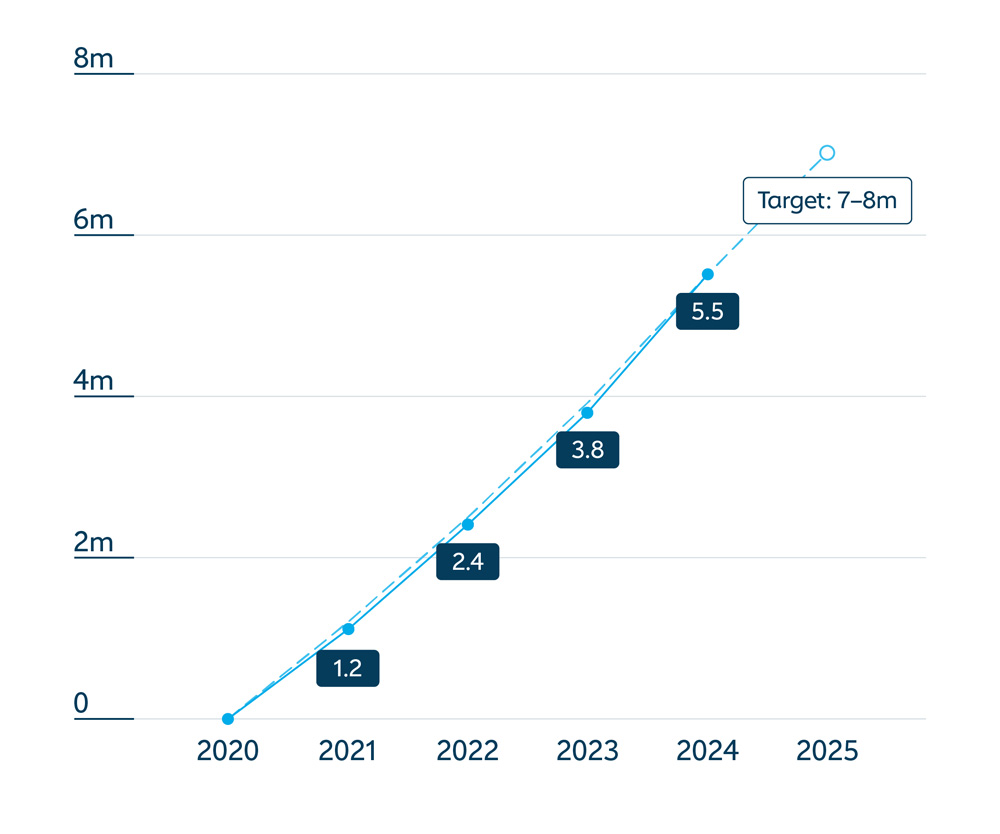

More than 59.8 million girls in lower-income countries are now protected against cervical cancer with Gavi support, preventing an estimated 1.2 million future deaths. By end 2024, 42 countries had launched their human papillomavirus (HPV) vaccine national programme with Gavi support (compared with 21 countries before the COVID-19 pandemic).

More girls in lower-income countries are protected against cervical cancer than ever before in history: more girls were fully immunised with HPV vaccine in 2024 than in the previous decade combined.

Vaccine focus: malaria vaccine

There are now two vaccines to protect against one of the biggest killers of young children on the African continent.

In December 2021, the Gavi Board made history by approving funding to support the roll-out of the world’s first malaria vaccine – nearly 35 years in development – in sub-Saharan Africa in 2022–2025. According to the World Health Organization (WHO), the vaccine is estimated to save 1 life for every 200 children vaccinated.

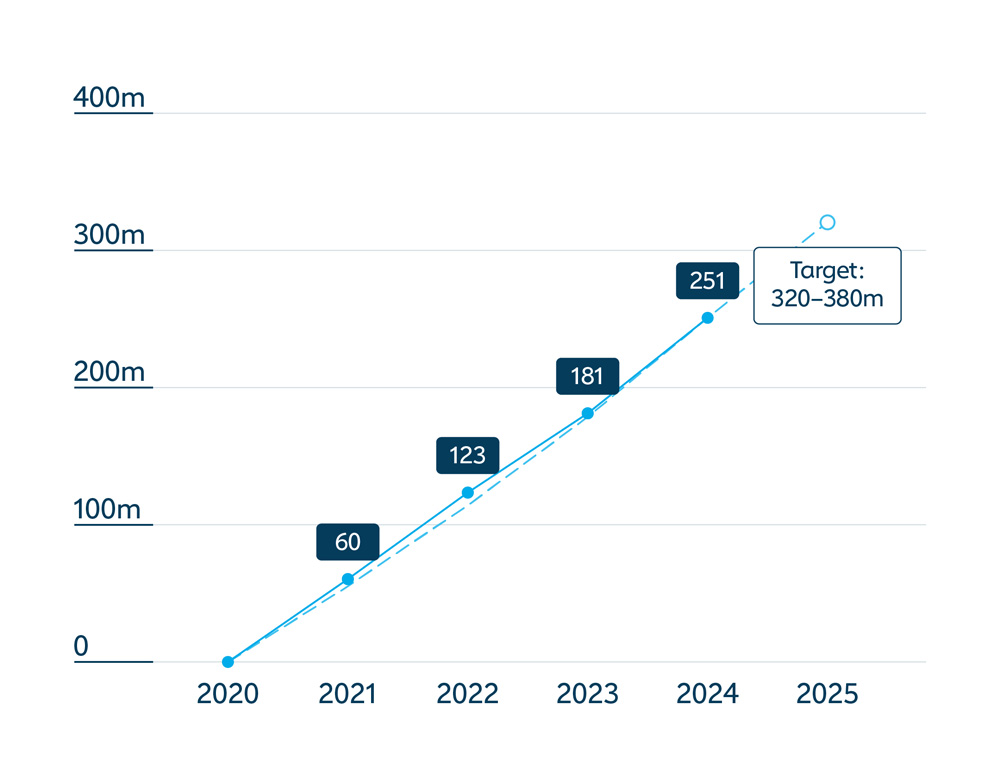

By end 2024, more than 10.54 million doses had been delivered to 17 countries in Africa which have introduced malaria vaccines into routine immunisation with Gavi support.

Since 2024, these countries have been funded under Gavi’s Malaria Vaccine Programme, aligning them with the other countries that have introduced malaria vaccines.

Sudan introduces the malaria vaccine

On 4 November 2024, in Gedaref, Sudan, Romisa Mohammad Ali holds her six-month-old daughter, Adan, the first child in Sudan to be vaccinated against malaria. “Vaccination is important to fight malaria. It is a dangerous disease, and children cannot tolerate it," says Romisa. "I tell all mothers that vaccination is safe, and I recommend that their children take the doses. This vaccination will protect our children.”

Credit: UNICEF/2024/Ahmed Mohamdeen Elfatih

The equity goal:

Strengthen health systems to increase equity in immunisation

Progress – 2024 equity updates: in 2024, health systems reached more children with Gavi-supported routine vaccines than ever before

With Gavi support for routine immunisation, lower-income countries protected more than 72 million children against a range of infectious diseases in 2024, more than any previous year on record – demonstrating the resilience of health systems in recovering from the COVID-19 pandemic.

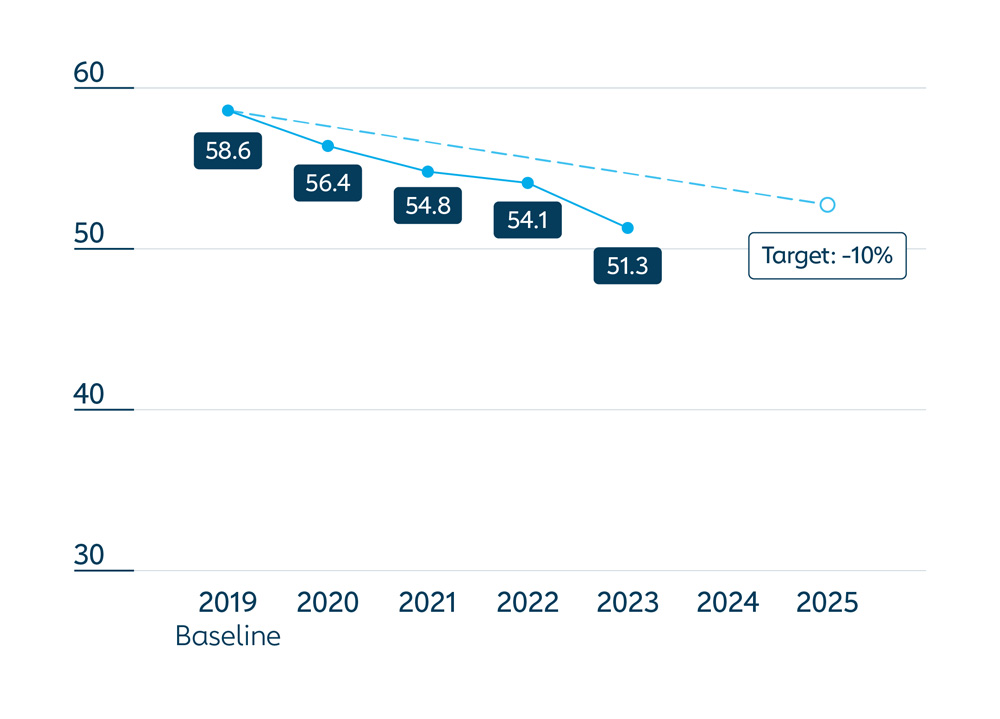

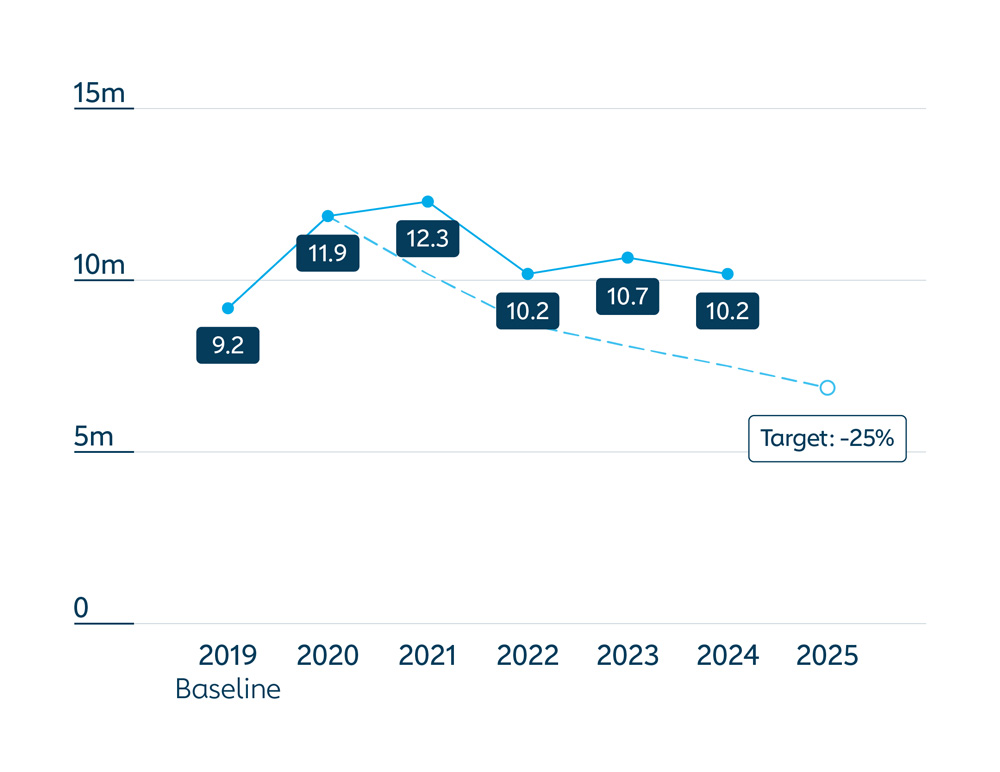

The number of zero-dose children in the 57 lower-income countries supported by Gavi decreased to 10.2 million children in 2024 (a reduction of 5% from 2023), while coverage of the third dose of diphtheria, tetanus and pertussis-containing vaccine (DTP3) increased to 82% in 2024 (up from 78% in 2021) – nearly back to pre-pandemic levels (i.e. 83% in 2019).

Even with an increasing birth cohort, African countries fully recovered DTP3 coverage to pre-pandemic levels – from 72% in 2022 back up to 76% in 2024.

children were reached with Gavi-supported routine vaccines in 2024 – more than in any year previously.

countries have installed more than 64,000 cold chain equipment (CCE) units procured by UNICEF Supply Division through Gavi’s CCEOP – nearly 2,700 in 2024 alone.

In 2024, Gavi-supported countries increased DTP3 coverage to 82% (compared to the 85% global average).

Reaching every child

"The Lao People’s Democratic Republic's commitment to digitising vaccine records in every one of the 1,081 health facilities sets an important example of how to harness innovation to leave no child behind."

Credit: Gavi/2024/Running Reel

72m

children in lower-income countries protected against a range of infectious diseases with Gavi support in 2024.

How Gavi’s co-financing model works

To bring countries on a trajectory towards financial sustainability, and to empower them to take ownership of their vaccination programmes, Gavi has pioneered an approach to co-financing and transition.

Countries share the costs of the vaccine programmes by directly co-procuring a portion of the vaccines and safe injection devices from a supplier or procurement agency to fulfil their co-financing requirements. As a country’s gross national income (GNI) per capita increases, so the level of its co-financing payments also rises. Countries are grouped under different categories according to their level of GNI per capita as a proxy of their ability to pay.

Learn more about Gavi co-financing

The sustainability goal

Improve sustainability of immunisation programmes

Progress – 2024 sustainability updates

Lower-income continued to prioritise immunisation investments in 2024, mobilising primarily domestic resources.

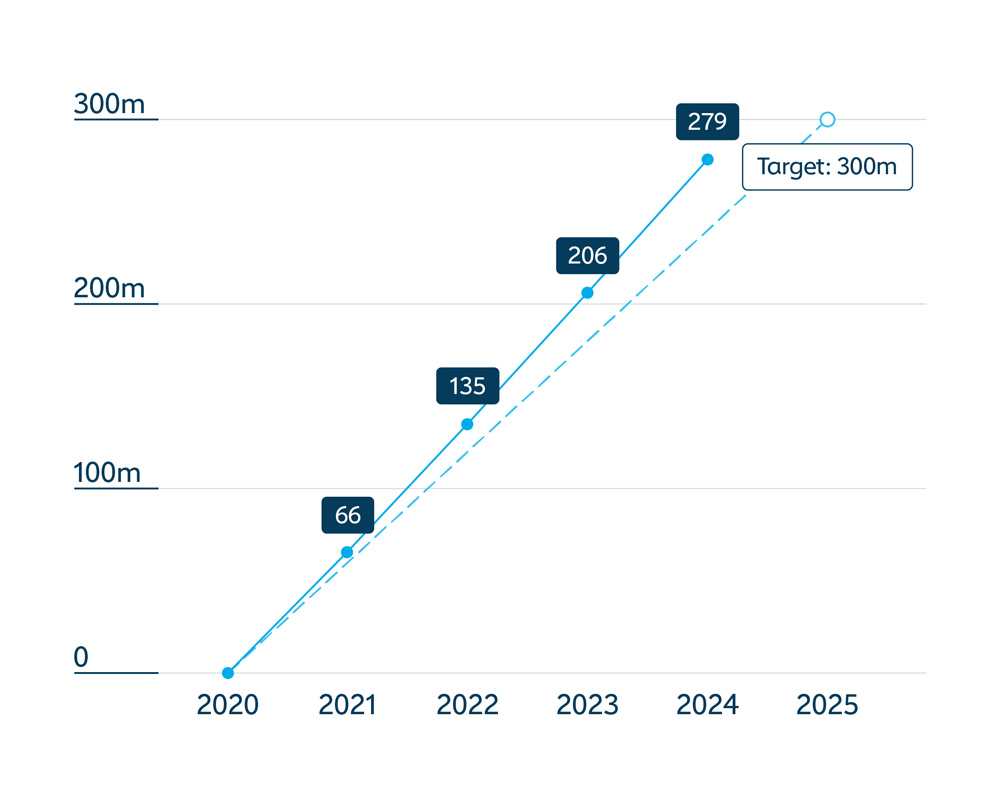

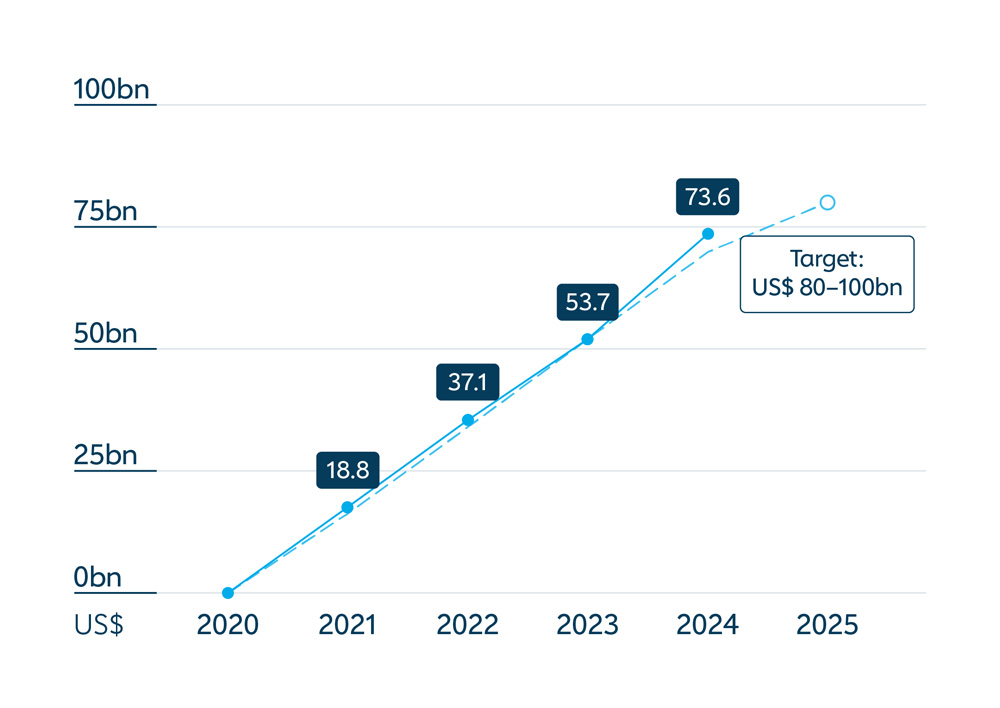

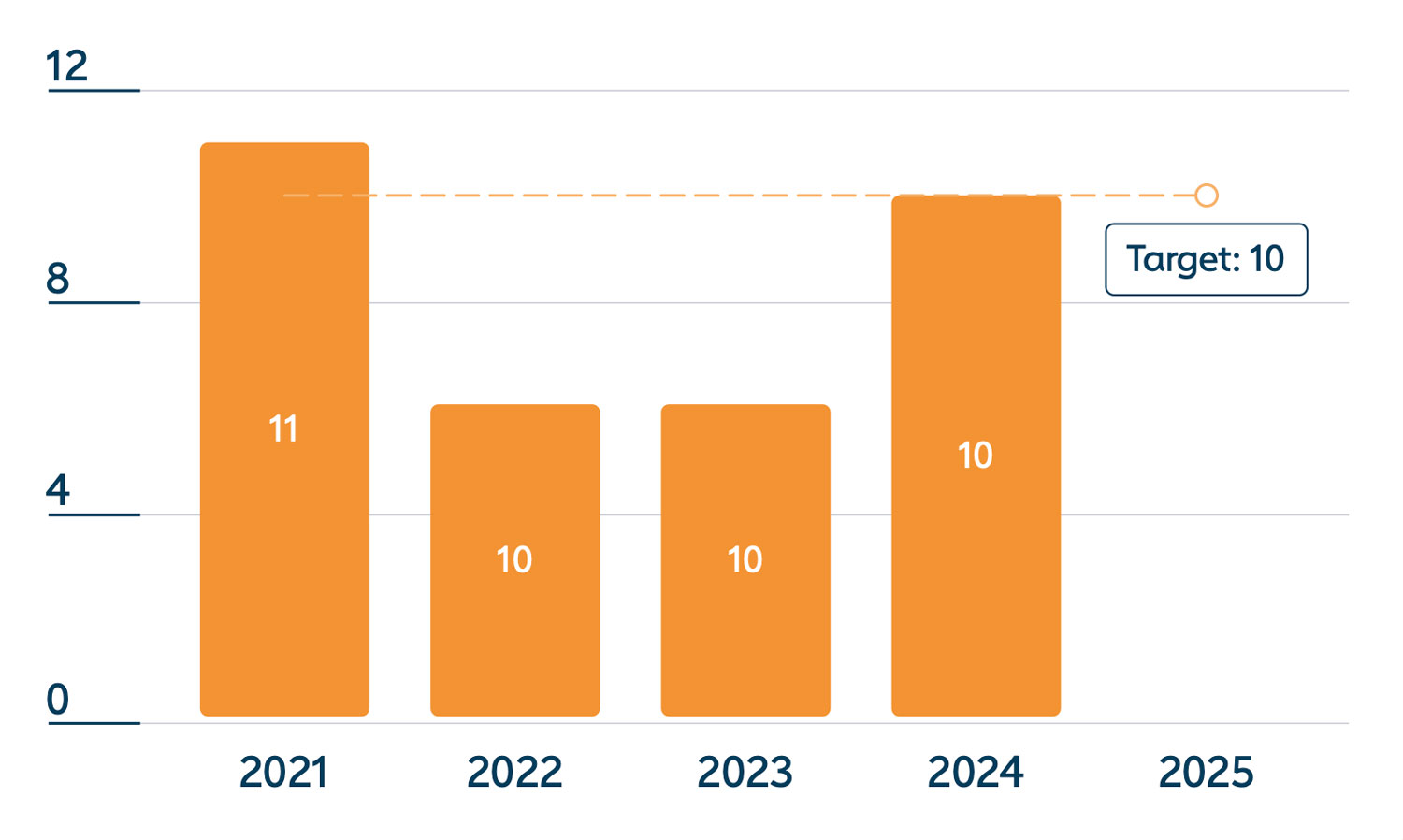

In a powerful demonstration of commitment to country ownership of immunisation, new data released in May 2025 showed that lower-income countries supported by Gavi, the Vaccine Alliance collectively contributed nearly US$ 255 million towards their own vaccination programmes in 2024 – a 19% increase from 2023.

was contributed by countries towards the cofinancing of Gavi-supported vaccines in 2024 – the highest amount yet and a testament to country ownership and the long-term financial sustainability of Gavi-supported vaccines.

vaccine programmes originally introduced with Gavi funding are self-financed by countries as of 2023, up from 40 in 2018.

of countries fully met their 2024 co-financing obligation – except six waivers for humanitarian crises.

In the face of fiscal challenges, climate change, conflict and instability, most Gavi-supported countries maintained or increased domestic resources for co-financing of Gavi-supported vaccines in 2024, bringing to US$ 1.9 billion their total contribution since the introduction of the co‑financing policy in 2008.

US$ 255m

Countries’ co-financing contributions in 2024 crossed the US$ 255 million mark for the first time – a 19% increase from 2023.

The healthy markets goal

Ensure healthy markets for vaccines and related products

Through Gavi’s market shaping efforts, the number of manufacturers supplying prequalified Gavi-supported vaccines reached 20 in 2024 (with nearly half based in low- and middle-income countries) – compared with 5 in 2001.

markets for vaccines and immunisation products exhibited acceptable levels of healthy market dynamics in 2024, meeting the target for the year.

innovative products were within the pipeline of commercial-scale manufacturers in 2024, continuing to exceed the Alliance target of 8 by 2025 well ahead of schedule.

mpox vaccine doses secured within a month of the WHO emergency declaration.

Mpox response

On 5 October 2024, UNICEF DRC Immunization Officer Dr Bijoux Bulindi receives the mpox vaccine during the official launch ceremony of the mpox vaccination campaign at Goma Provincial Hospital, North Kivu province, Democratic Republic of the Congo (DRC).

“I decided to be among the first to get vaccinated because I am conducting mpox epidemiological surveillance in the field and I want to lead by example,” Dr Bijoux said.

US$ 1.2bn

available over ten years to support the sustainable growth of Africa’s manufacturing base.

African Vaccine Manufacturing Accelerator (AVMA)

In June, Gavi launched the African Vaccine Manufacturing Accelerator (AVMA), a financing instrument that will make up to US$ 1.2 billion available over ten years to support the sustainable growth of Africa’s manufacturing base. At the same time, Gavi and UNICEF launched a vaccine market dashboard to guide investment decisions with real-time supply-demand insights.

Healthy market dynamics

2024 progress: on track

Healthy market dynamics are assessed via analysis of fundamental market attributes: demand side dynamics, supply side dynamics and innovation. This holistic view of markets aligns market shaping activities and objectives with Gavi’s strategic goals to: introduce and scale up vaccines; and improve sustainability of immunisation programmes.

2024 progress: Gavi’s ongoing market shaping efforts and collaborations with manufacturers helped ensure that ten vaccine markets exhibited acceptable levels of healthy market dynamics, the same number as in 2023 and in 2022.

Data sources: vaccine procurement data: UNICEF SD Memorandum of Understanding (MoU) reports; market intelligence data: Gavi Market Shaping roadshows, Alliance partner industry engagements, 2025

Gavi's progress report 2024

Highlighting key data, partnerships and milestones, the 2024 Annual Progress Report offers insights into our progress last year, while facing the challenges ahead.

Previous progress reports

Welcome to Gavi’s 2023 Annual Progress Report, the third of the 2021–2025 strategic period.

Welcome to Gavi’s 2022 Annual Progress Report, the second of the 2021–2025 strategic period.

Welcome to Gavi’s 2021 Annual Progress Report, the first of the 2021–2025 strategic period.