Annual Progress Report 2018

Welcome to Gavi’s 2018 Annual Progress Report, the third in a series of five covering this strategic period. The report shows we are seeing continued positive progress, with countries reaching more children with a greater number of Gavi-supported vaccines. But it also identifies some challenging new trends which suggest that if we are to continue to make progress in our next strategic period, then a new approach is needed.

Dr Seth Berkley, CEO

Since 2016 we have helped immunise nearly 200 million more children and are ahead of our mission target to reach 300 million children by 2020.

In the 68 Gavi-supported countries the proportion of children receiving a first dose of a measles vaccine has risen by 3 percentage points, signalling that we are on track for that target. The breadth of protection has also increased, by 10 percentage points in the last year alone and 21 percentage points since the beginning of this strategy period. And the sustained progress in coverage of several new vaccines, including pneumococcal, rotavirus, inactivated polio and rubella containing vaccines, also speaks to the successful vaccine introduction and scale-up efforts. All this, and the progress Gavi has made in strengthening immunisation programmes, delivery systems and surveillance systems, as well as boosting vaccine stockpiles are helping to safeguard against disease outbreaks and reduce the threats to global health security, making the world a safer place for everyone.

However, despite immunising more children, 4% more in 2018 compared with 2015, the latest data suggests that the proportion of children receiving all three doses of DTP vaccines has plateaued during this period. This is partly due to acute problems that a small number of previously high performing countries have faced. But even taking this into account, it is now clear that shifts in population growth trends are presenting growing challenges.

Since Gavi was created it has consistently succeeded in increasing coverage despite sustained population growth in Gavi-supported countries. But now because fertility rates are higher in fragile or conflict-affected countries, Gavi is facing a growing challenge as these are typically countries with weak health systems. So, as wealthier countries continue to transition out of Gavi support, the proportion of those remaining that are fragile will increase. This means that the number of children born annually in the countries that Gavi will support throughout the next strategy period is now expected to grow twice as fast. Because of this, just sustaining coverage, let alone achieving our ambition to increase coverage, will become more difficult.

The good news is that, as indicated in this report, in such countries, Gavi’s investments in health system strengthening, provision of higher level of technical support and greater political engagement are paying off. Through this kind of increased investment, and a stronger focus on targeting communities and countries with low coverage and a high number of underimmunised children, we are seeing greater progress.

As the Gavi Board devised its strategy for the 2021–2025 strategic period, all this has helped serve as a backbone to a new approach which will help us make the last mile our first priority. With equity an organising principle, this new strategy, Gavi 5.0, will give an greater emphasis on providing differentiated, tailored and targeted support for countries. The enhanced focus on gender, communities, demand and innovation, and the increased support in prioritising high impact vaccines, and more vaccines, will enable us to reduce the number of children who receive no vaccines at all. And through our continued market shaping efforts and a bigger focus on programmatic sustainability and post-transition support, we will reduce the risk of backsliding and allow us to prevent millions of vulnerable children from missing out even if they don’t live in Gavi-supported countries.

All this stands us in good stead to not only meet our goals for the current period but to tackle these growing challenges, and whatever new ones we face, in the coming years. Adaptability is at the core of Gavi’s business model, and so our ability to evolve will enable us to continue to make positive progress, safeguard the world and ensure that no one is left behind.

Dr Ngozi Okonjo-Iweala, Board Chair

For Gavi, one of the most notable highlights of 2018 was a marked increase in the level of country-ownership.

This sends a positive signal that governments are increasingly recognising how investing in health can not only help lift vulnerable communities out of poverty, but that it’s also good for the economy. For Gavi this is a critical part of its mission to reach more children, because we cannot do it without them.

One clear indication of this was the level of domestic investment in immunisation, with 94% of Gavi-supported countries paying their co-financing obligations by the end of 2018 – the highest proportion since co-financing was introduced. Similarly, with 16 countries now having transitioned out of Gavi support and fully-financing their vaccination programmes, we have seen 40 new vaccine introductions fully-financed by the governments of transitioned and transitioning countries.

With a total of US$ 124 million invested in co-financing and US$ 283 million in self-financed vaccine programmes, this not only represents a clear commitment by governments, but also demonstrates how the Gavi model of helping countries to build and fund sustainable immunisation programmes really does work.

However, with one in ten children still not receiving a full course of a basic diphtheria-tetanus-pertussis-containing vaccine we need to do more. That means stepping up our political engagement, to get ministers of health and finance on board, and intensifying efforts to identify and reach pockets of inequity that exist within countries. But in addition to this, with more countries seeking support to help boost demand, we are now also looking at what more can be done at the community level.

One issue that will become an increasing focus in Gavi’s next strategic period, is how we can address the gender-related barriers that can often act as obstacles to improving access to immunisation. Whether cultural, social or religious, it has become clear that such barriers can play a major role in preventing female caregivers, on whom the responsibility often falls, from getting their children immunised. By ensuring service delivery is sensitive to such barriers, such as through the improved interpersonal communications of frontline health workers or by increasing awareness through continued community engagement, we can address these barriers and ensure no one is left behind.

Whether it is at the government or the community level, country engagement is key to Gavi’s continued progress. It seems quite appropriate then that Gavi’s 2020 London Replenishment is launched this year surrounded by African Heads of State and Ministers at the 7th Tokyo International Conference on African Development, an event that was originally created to promote Africa’s development, peace and security. While Gavi is on track to achieve its current targets, its long-term success does not just rest with donor and Alliance partner support. Ultimately, it is only by empowering countries that we can protect the lives and the futures of the next generation.

Measuring our performance

Measuring our performance

mission and strategic goals

The Vaccine Alliance’s 2016–2020 mission is to save children’s lives and protect people’s health by increasing equitable use of vaccines in lower-income countries.

Five mission indicators reflect our overall aspiration for the 2016–2020 period. They measure our impact on numbers of immunised children, future deaths prevented, under-five mortality rates and years lost due to disability or death in the countries we support.

We also track what proportion of countries successfully maintain all their recommended vaccine programmes after our financial support stops – a reflection of our strategy’s increasing emphasis on ensuring sustainability of immunisation.

Mission indicators

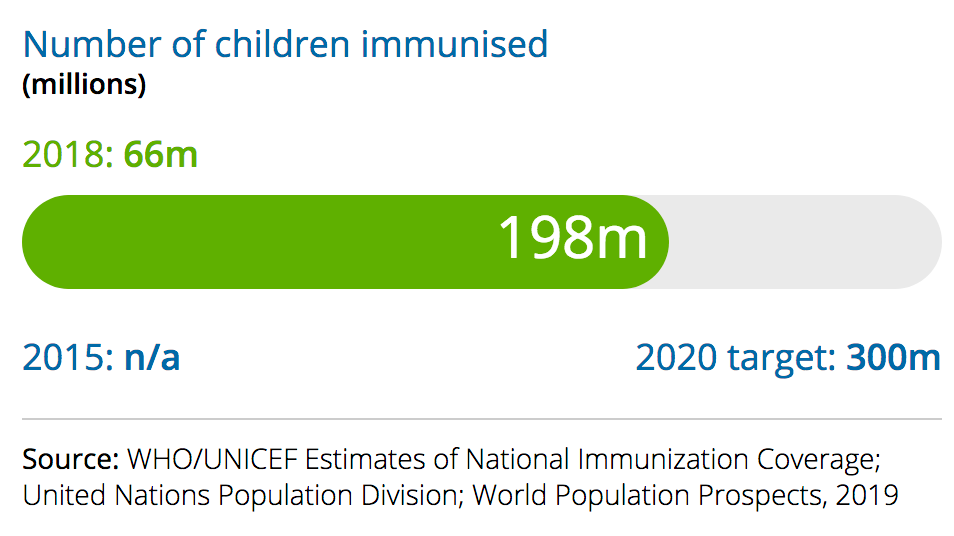

Children immunised

What we measure

The number of children immunised with the last recommended dose of a Gavi-supported vaccine delivered through routine systems.a People immunised through campaigns and supplementary immunisation activities are not included.

2018 performance

Countries immunised 66 million additional children in 2018 – often with more than one Gavi-supported vaccine. Although this is down from 67 million in 2017, Gavi is still on track to help countries immunise an additional 300 million children in the 2016–2020 strategy period. 198 million unique children have been immunised between 2016 and 2018.

a – To ensure that we do not double-count children who receive more than one vaccine, we only take into account the Gavi-supported vaccine with the highest coverage level in each country.

Future deaths prevented

What we measure

The number of anticipated future deaths prevented as a result of vaccination with Gavi-funded vaccines in the countries we support.

2018 performance

Countries prevented approximately 1.7 million future deaths in 2018, thanks to Gavi-supported vaccines. Together with the approximately 1.3 million averted deaths in 2017, this puts us well on track to help countries avert 5–6 million future deaths in the 2016–2020 period.

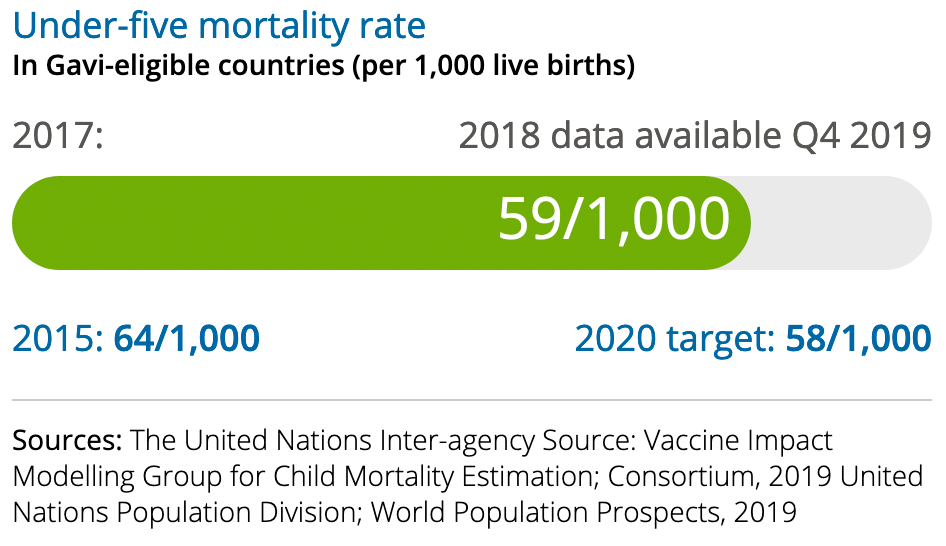

Under-five mortality rate

What we measure

The average probability of a child born in any of the Gavi- supported countries dying before they reach the age of five.

2018 performance

The under-five mortality rate fell from 61 to 59 deaths per 1,000 live births between 2016 and 2017, putting us on track to reach our target of 58 deaths per 1,000 live births by the end of 2020. 2018 estimates will be available in late 2019.

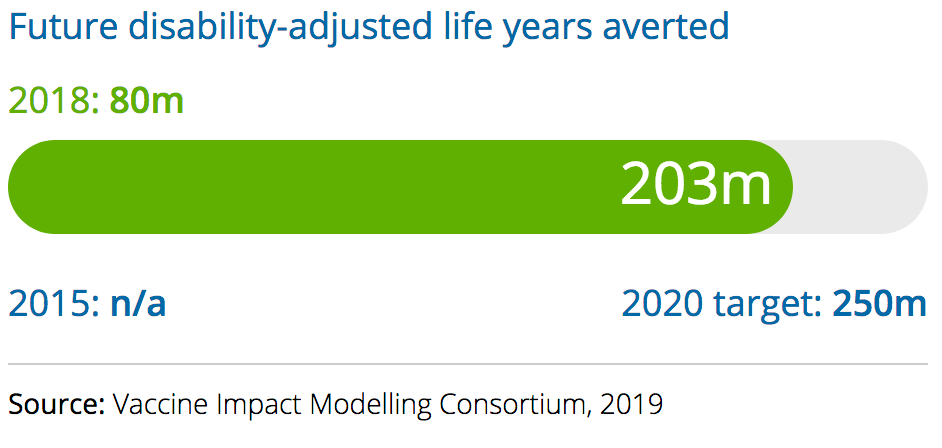

Future disability-adjusted life years averted

What we measure

The number of anticipated future disability-adjusted life years (DALYs) averted as a result of vaccination with Gavi-supported vaccines. DALYs measure the number of healthy years lost due to disability or premature death.

2018 performance

Countries averted approximately 80 million DALYs in 2018 thanks to our support, having averted approximately 63 million in 2017. We are on course to achieve our target of 250 million DALYs averted by 2020.

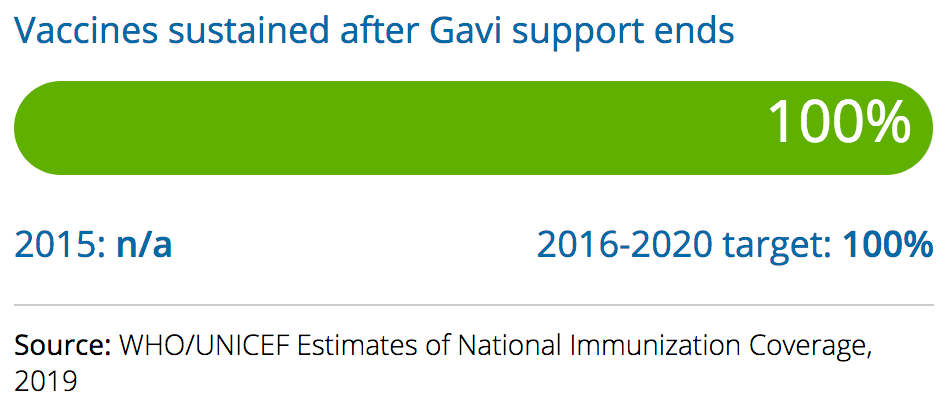

Vaccines sustained after Gavi support ends

What we measure

The percentage of countries that continue to deliver all recommended vaccines included in their routine programmes after they transition out of Gavi financing. This indicator covers all vaccines recommended by national authorities for routine immunisation, not only those supported by Gavi.

2018 performance

All transitioned countries continued to deliver all their recommended routine vaccination programmes throughout 2018.

Four strategic goals and a set of key performance indicators help us track our progress

Four strategic goals and a set of key performance indicators help us track our progress

The vaccine goal

Performance indicators

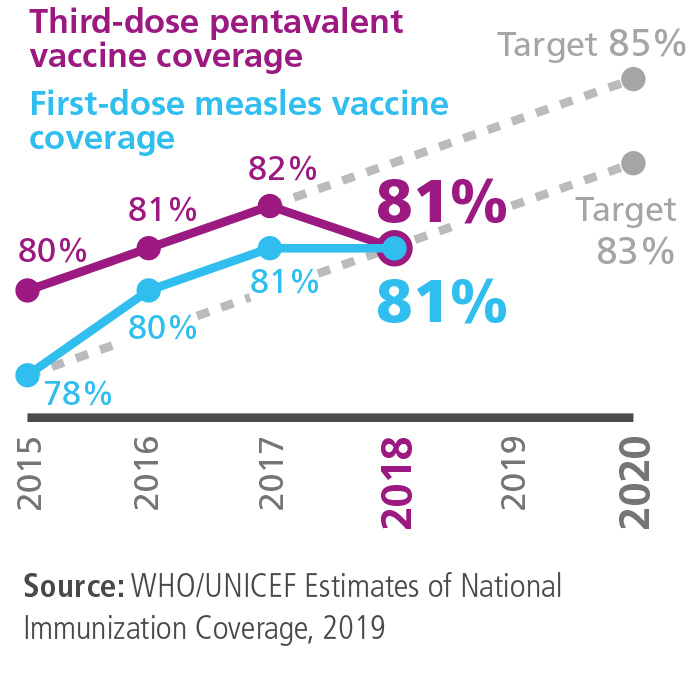

Routine immunisation coverage

What we measure

Percentage of children reached with the third dose of pentavalent vaccine, which protects against diphtheria, tetanus, pertussis (DTP3), hepatitis B and Hib, and the first dose of measles vaccine in Gavi-supported countries. These two vaccines are included in the routine schedules of all Gavi-supported countries. Coverage estimates for both provide a reliable indicator of the proportion of children with access to basic immunisation services.

2018 performance

Average coverage of the first dose of measles vaccine in Gavi-supported countries has plateaued at 81%. While third-dose pentavalent vaccine coverage increased between 2015 and 2017, it has since fallen slightly – leaving us off track to reach our 2020 target.

This stationary trend is particularly evident in the 16 countries classified as fragile, where coverage has remained at just 73% since 2014. Four transitioned countries saw coverage fall in 2018 – a reminder that even countries that transition with high coverage may backslide.

As a result of population growth and despite flatlining coverage rates, countries are continuing to immunise the same number of children as before. The total number of children who received a third dose of DTP-containing vaccine in Gavi-supported countries held steady at over 64 million in 2018.

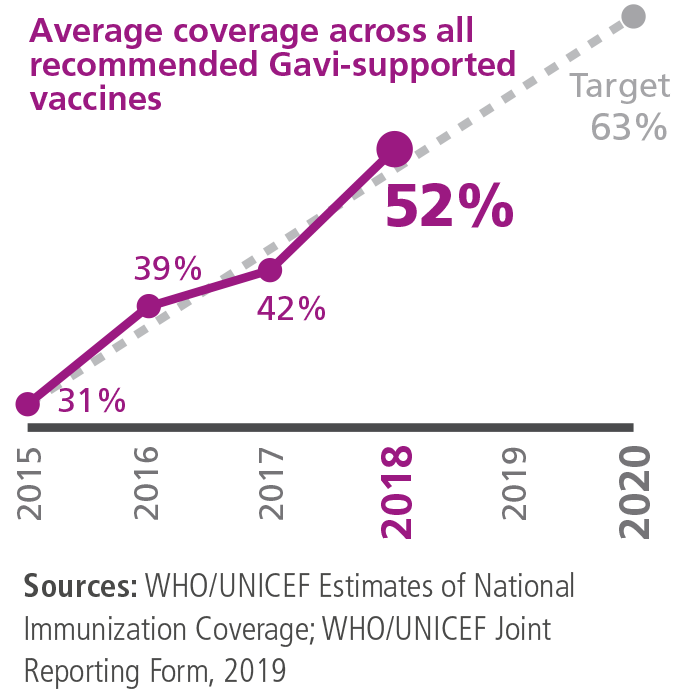

Breadth of protection

What we measure

Percentage of children reached with the last dose of vaccines recommended across all Gavi-supported countries and the last dose of three vaccines specific to certain regions.a

2018 performance

Coverage for these vaccines averaged 52% in 2018, an increase of 10 percentage points compared with 2017. Progress was in line with our target in 2018 – and we are on track to reach our 2020 target of 63%.

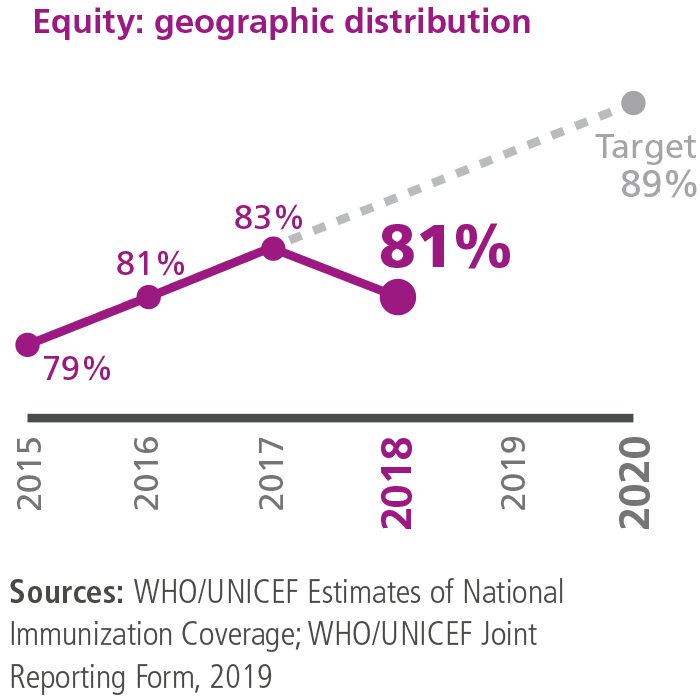

Equity: geographic distribution

What we measure

Average percentage of districts across the countries we support in which coverage with a third dose of pentavalent vaccine is equal to or greater than 80%. As part of an increased effort to ensure accurate subnational data is available for measuring equity, WHO and UNICEF have started to report geographically disaggregated coverage data on an annual basis.

2018 performance

The proportion of districts in Gavi-supported countries in which coverage of three doses of pentavalent vaccine is equal to or above 80% dropped from 83% in 2017 to 81% in 2018. We are currently not on track to achieve our 2020 target of 89%. This indicator does not cover the same set of countries each year, so tracking progress is challenging.

The Alliance works as part of the newly-formed Equity Reference Group (led by the Gates Foundation and UNICEF), which aims to generate innovative ideas to accelerate progress on equity in immunisation across four key contexts: urban poor, remote/rural areas, conflict and gender-related barriers. The group has started making recommendations for global and national decision-makers.

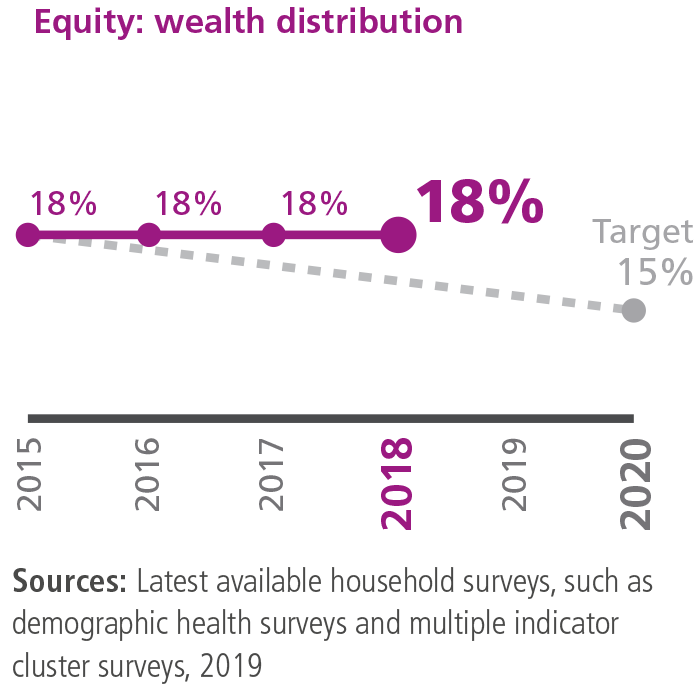

Equity: wealth distribution

What we measure

Average difference in coverage with a third dose of pentavalent vaccine between the poorest 20% of the population and the richest 20% across the Gavi-supported countries where recent data is available.

2018 performance

The average difference between immunisation coverage in the richest and poorest quintiles in Gavi-supported countries has remained at 18% since 2015. The lack of movement on this indicator means that we are not on track to reach our 2020 target of 15%.

However, some positive trends were observed in 2018. Four out of eight countries with new surveys reported reduced inequity across income groups. For instance, Guinea, Pakistan and Senegal showed an average reduction in wealth inequity of 12 percentage points. Due to the low availability of recent data, accurately measuring changes remains difficult.

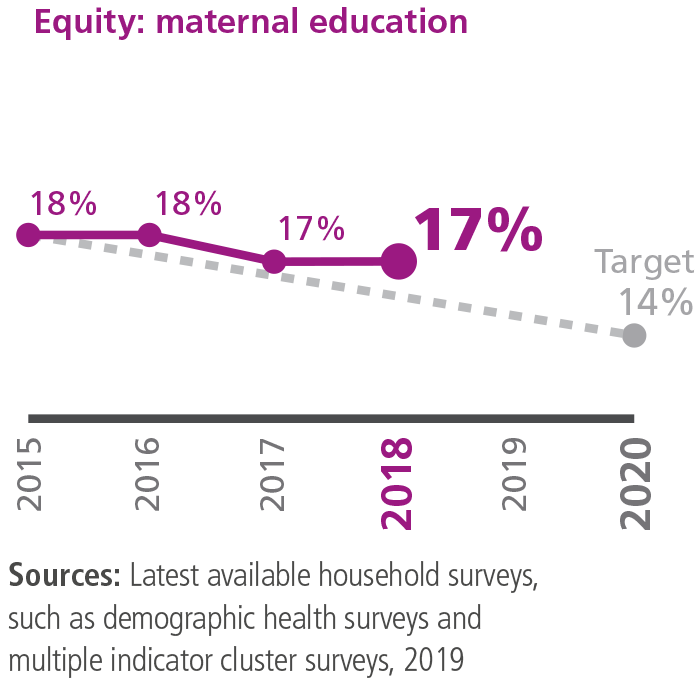

Equity: maternal education

What we measure

Average difference in coverage between children of non-educated mothers or other female caregivers, and those whose mothers have at least completed secondary school. We use three doses of pentavalent vaccine as the basis for this indicator, which includes all Gavi-supported countries where recent survey data is available.

2018 performance

The average difference between coverage of the third dose of pentavalent vaccine among children of educated and non-educated mothers in Gavi-supported countries has stalled at 17% – just one percentage point below the 2015 baseline. Recent surveys in Guinea, Pakistan and Senegal showed an average drop in maternal education inequity by eight percentage points; we will need similar levels of progress across more countries to reach our 2020 target of 14%.

The lack of availability of recent data makes it difficult to track this indicator accurately.

The health systems goal

The health systems goal

increase the effectiveness and efficiency of immunisation delivery as an integrated part of strengthened health systems

Performance indicators

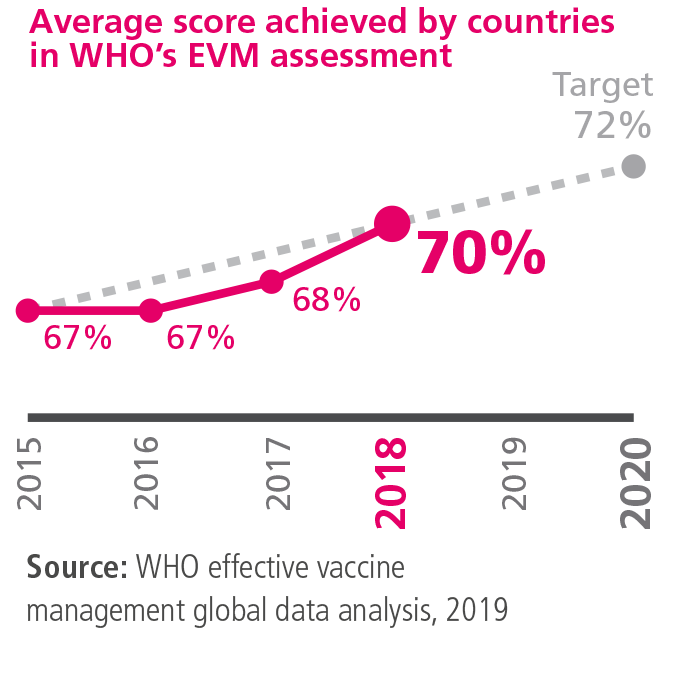

Supply chain performance

What we measure

The average score achieved by Gavi-supported countries that have completed WHO’s effective vaccine management (EVM) assessment. This indicator helps countries to evaluate their immunisation supply chain performance over time against best practice standards, as well as to identify and respond to shortcomings. Among the features assessed are vaccine management, storage capacity, human resources and information systems.

Strong supply chains are essential for counties to ensure vaccines are available wherever and whenever they are needed, and that they are stored consistently at the temperatures required to remain potent and safe.

2018 performance

Gavi-supported countries achieved an average EVM score of 70% in 2018, up from 68% in 2017. We are on track to achieve the agreed 2020 target of 72%. All nine countries that conducted a new EVM assessment in 2018 showed an improvement in their composite score, with an average improvement of 11 percentage points. 25% of countries had EVM scores equal to or above 80% – the WHO-defined standard for a well-functioning supply chain – compared with 15% in 2016.

Most of the recent improvements were seen in the four areas targeted by Gavi investments: storage and transport; buildings and equipment; vaccine management; and maintenance.

The Alliance is working with a range of private-sector partners to introduce innovative supply chain solutions, including drone vaccine delivery and cutting-edge temperature monitoring devices.

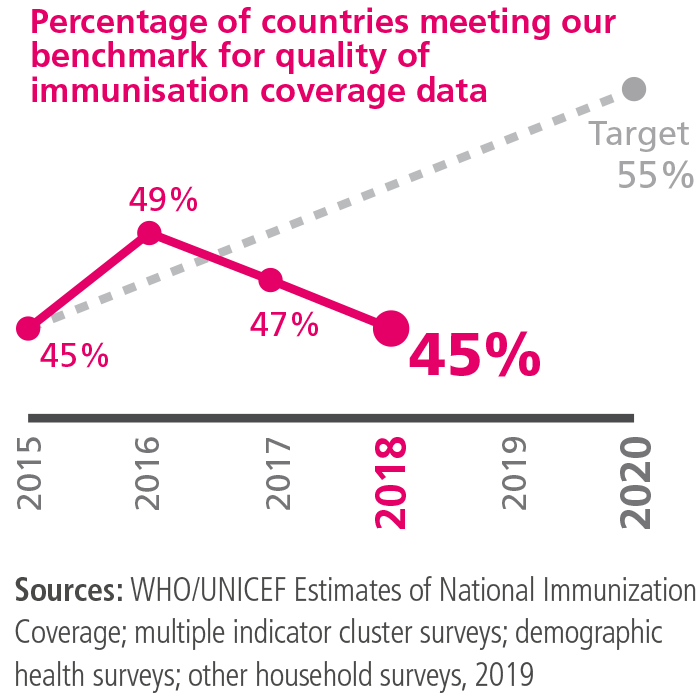

Data quality

What we measure

Proportion of Gavi-supported countries with a less than 10 percentage point difference between different estimates of immunisation coverage.

This indicator reflects the degree of consistency between available estimates of immunisation coverage. “Administrative coverage” refers to estimates based on national-level data reported annually by the country itself. “Survey coverage” refers to estimates based on data collected as part of household surveys, such as the demographic health survey, which is usually carried out every three to five years.

2018 performance

45% of countries reported administrative coverage data within 10 percentage points of survey coverage, compared with 47% in 2017. This means that we are off track to achieve our 2020 target of 55%.

Revisions of previous years’ coverage estimates in the latest WHO/UNICEF Estimates of National Immunization Coverage (WUENIC) are a reminder that measurement remains a key challenge. In a continued effort to improve data quality, and with support from Gavi’s data strategic focus area, WHO and UNICEF are conducting a review of the WUENIC methodology, including comparisons with multiple alternative methods.

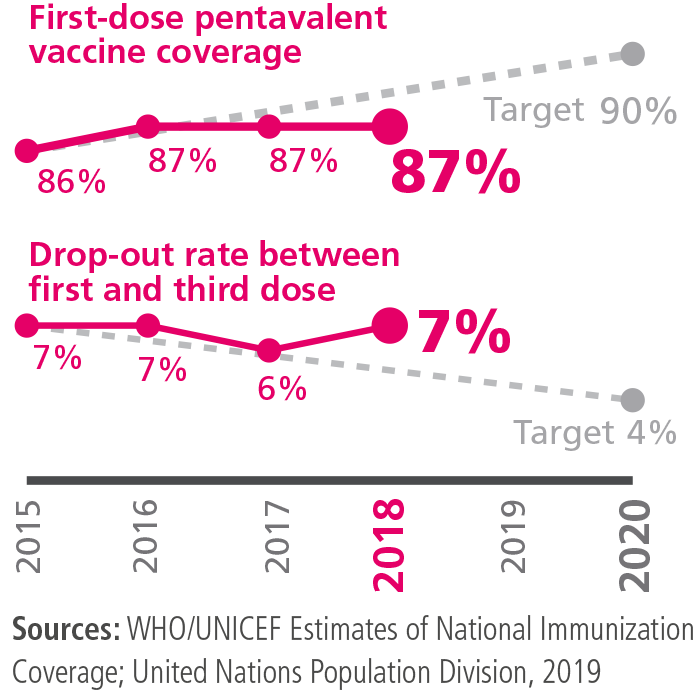

Coverage with a first dose of pentavalent vaccine and drop-out rate between the first and third dose

What we measure

Coverage with a first dose of pentavalent vaccine and the drop-out rate between the first and third dose in countries we support.

Taken together, these two measures provide a good indication of the ability of the health system to deliver immunisation services. High first-dose coverage coupled with low rates of drop-out from the first to the third dose suggest a strong health system, capable of reaching and fully immunising children with the required number of doses. A weaker delivery system may succeed in reaching a child with the first dose but not the third.

2018 performance

Coverage with a first dose of pentavalent vaccine in Gavi-supported countries remained at 87% for the third successive year, having increased from 86% in 2015. We are not on track to reach our 2020 target of 90%.

The drop-out rate was 7%, compared with 6% in 2017. We are off track to achieve our target of 4% for this indicator.

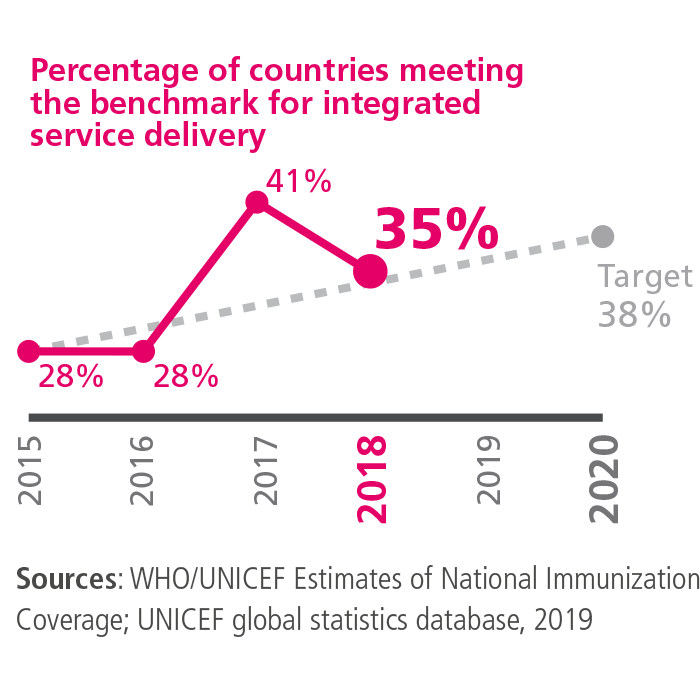

Integrated health service delivery

What we measure

Percentage of countries we support meeting our benchmark for integrated delivery of antenatal care and immunisation services.

A country meets this benchmark if coverage levels for four interventions – antenatal care and administration of neonatal tetanus, pentavalent and measles vaccines – are within 10 percentage points of each other, and all above 70%.

If these complementary services are achieving similar levels of coverage, it generally follows that the linkages and coordination between them are strong.

2018 performance

Some progress has been made in this area but this year the measure slipped back to 35% from 41% the previous year, and below the target of 38% for 2020.

Gavi fully promotes integrated approaches combining, for example, rotavirus, pneumococcal, human papillomavirus and measles programmes with comprehensive plans to reduce the burden of diarrhoea, pneumonia and cervical cancer. Gavi’s support for measles campaigns also helps to deliver vitamin A and deworming. Support for the cholera vaccine stockpile also strengthens multisectoral disease control efforts. Future vaccines in the VIS bring more opportunities for integrated multisectoral approaches.

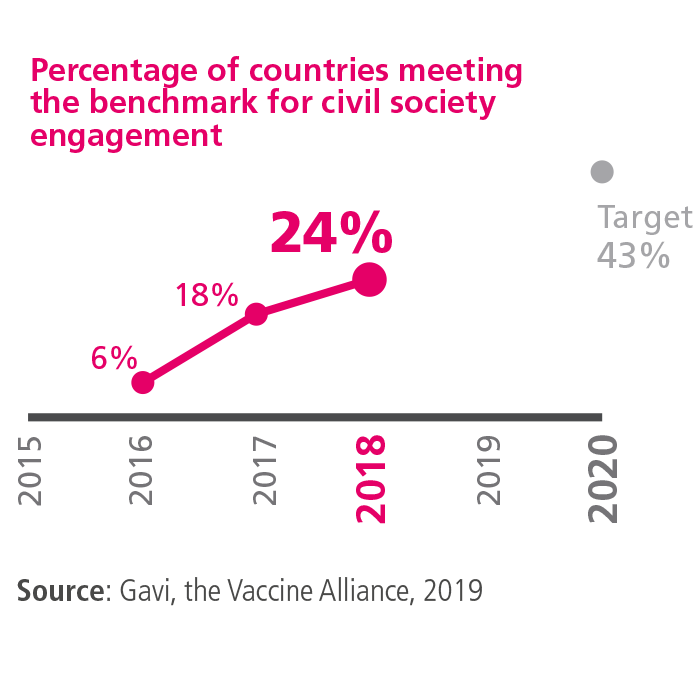

Civil society engagement

What we measure

Percentage of countries we support that meet our benchmarks for civil society engagement in national immunisation programmes to improve coverage and equity.

We use three criteria to assess the level of civil society engagement:

- inclusion of civil society organisations (CSOs) in national immunisation plans with clearly stated activities;

- defined allocations in the Expanded Programme on Immunization (EPI) budget for CSO plans and activities (or justification given as to why these are not included); and

- documented evidence that CSO plans have been completed and/or are being implemented.

2018 performance

24% of Gavi-supported countries met all three criteria, up from 18% in 2017. However, we are not on track to meet the target of 43% in 2020.

The sustainability goal

Performance indicators

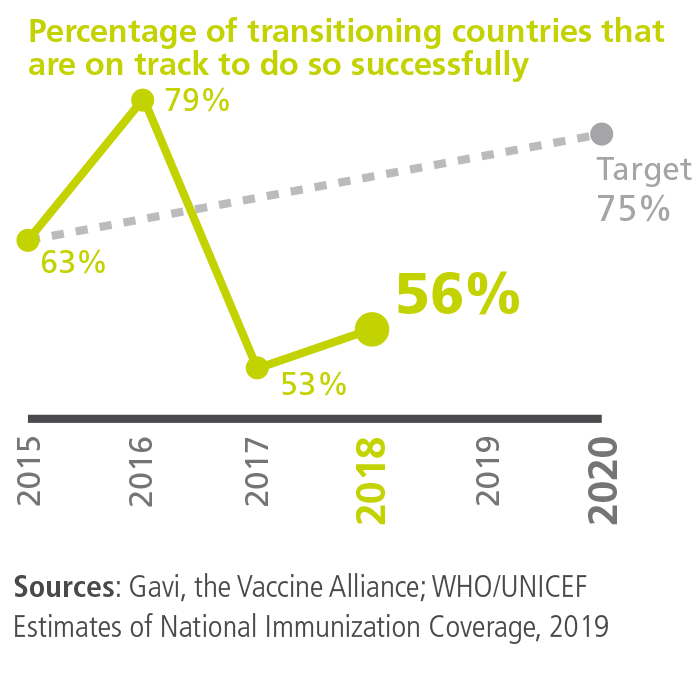

Countries on track to successful transition

What we measure

percentage of countries in the accelerated transition phase that are on track to transition successfully. A country is on track if:

- at least 75% of predefined transition activities (such as a having a functional national regulatory agency) have been completed on time;

- DTP3 coverage has increased over the last three years (if a country has already achieved at least 90% DTP3 coverage, this level should have been sustained for three years); and

- it is meeting its co-financing obligations and did not default on payments in the previous year.

2018 performance

By the end of the year, 56% of countries in the accelerated transition phase were on track to transition successfully. While this is below the target of 75%, the countries that missed the criteria – Nigeria, Papua New Guinea, Solomon Islands and Vietnam – did so because of low coverage. An alternative calculation which includes all the transitioned and transitioning countries shows a better performance of 70%.

Nigeria and Papua New Guinea now have tailored transition strategies with targeted investments to improve coverage outcomes. A 19 percentage point decline in coverage in Vietnam in 2018 was the result of a pentavalent product switch and associated supply shortages which have now been resolved. For the Solomon Islands, the 2018 coverage figure of 85% is below a reported figure of 94% for 2016, but is more or less in line with a newly published estimate of 83% for 2017.

In total, transitioning and transitioned countries fully self-financed 40 vaccine programmes, compared to 27 in 2017. Countries’ self-financing in 2018, combined with India’s co-financing contributions, amounted to US$ 301 million – a substantial increase from US$ 160 million in 2017. This increase is largely driven by India where catalytic support has helped unlock domestic financing, with the country self-financing US$ 238 million in 2018, up from US$ 112 million in 2017.

By the end of 2018, 16 countries – Angola, Armenia, Azerbaijan, Bhutan, Bolivia, Congo, Cuba, Georgia, Guyana, Honduras, Indonesia, Kiribati, Mongolia, Republic of Moldova, Sri Lanka and Timor-Leste – had transitioned out of our support.

As of January 1st 2019, Congo will regain eligibility and Syria, which has never been a Gavi country, will become eligible for Gavi support.

All transitioned countries are fully financing all vaccine programmes introduced with Gavi support and 11 of these countries have already achieved DTP3 coverage rates of 90% or above.

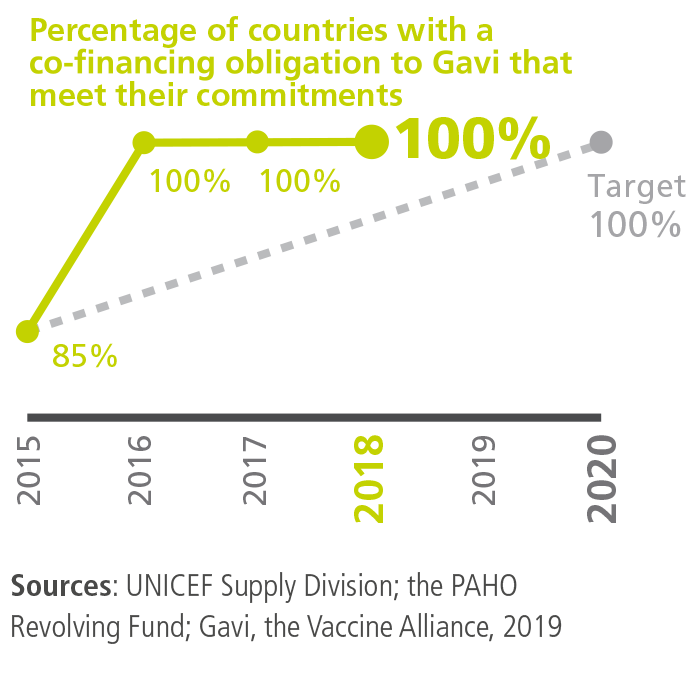

Co-financing

What we measure

Percentage of countries that fulfil their co-financing commitments by the end of the year, or which pay their arrears in full within 12 months.

2018 performance

All countries met their 2017 co-financing commitments in that year or paid all their arrears in 2018. In addition, 49 out of 52 countries (94%) fulfilled their 2018 obligations in a timely manner.

Only three countries – Cameroon, Ghana and Sierra Leone – defaulted on their 2018 payments, the lowest proportion since the co-financing policy was introduced. The Alliance will step up its engagement with all three countries in 2019 to help develop tailored plans for payment of the arrears and mitigate the risk of future defaults. Collectively, countries paid 95% of their co-financing obligations before the end of 2018 (compared with 90% the year before) and co-financed or self-financed 226 programmes – up from 197 the previous year.

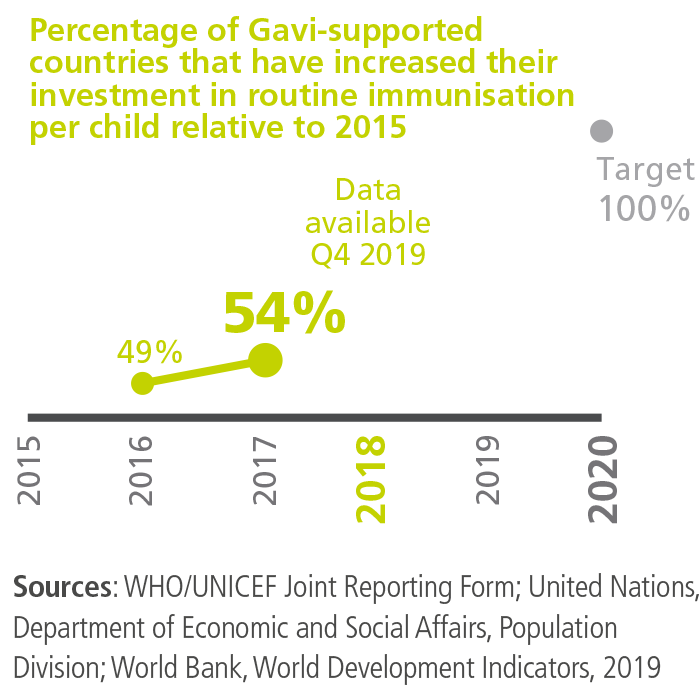

Country investments in routine immunisation

What we measure

Percentage of countries that have increased their investment in routine immunisation per child, relative to 2015. This indicator takes into account every vaccine in a country’s national programme, not just those supported by Gavi. It also includes expenditure on related products, such as injection supplies.

2018 performance

54% of Gavi-supported countries increased their investment in routine immunisation between 2016 and 2017. Data for 2018 will be available in November 2019. The target for 2020 is that immunisation investment per child will have increased in all Gavi-supported countries.

Other sources also show evidence of growing vaccine investments in low-income countries. For instance, the 2018 Global Vaccine Action Plan (GVAP) Report showed a 130% increase in government expenditure in the African region since 2010.

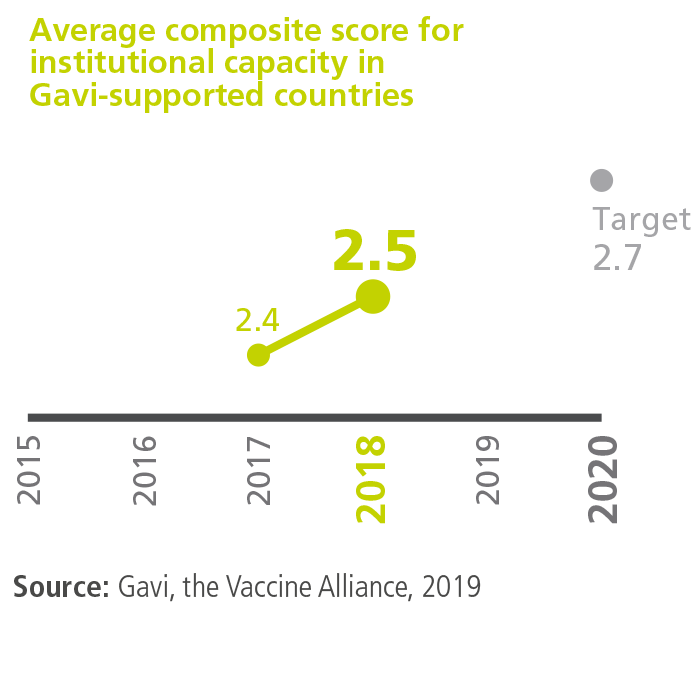

Institutional capacity

What we measure

Average score of Gavi-supported countries measured against our criteria for national decision-making, programme management and monitoring. Through this indicator, we assess the performance and effectiveness of bodies that manage immunisation, including the Expanded Programme on Immunization (EPI), interagency coordinating mechanisms and national immunisation technical advisory groups (NITAGs).

2018 performance

Gavi-supported countries achieved an average score of 2.5 out of a maximum 4.0 in the institutional capacity assessment, up from 2.4 in 2017. This means that the Alliance is on track to reach its 2020 target of 2.7.

The market shaping goal

Performance indicators

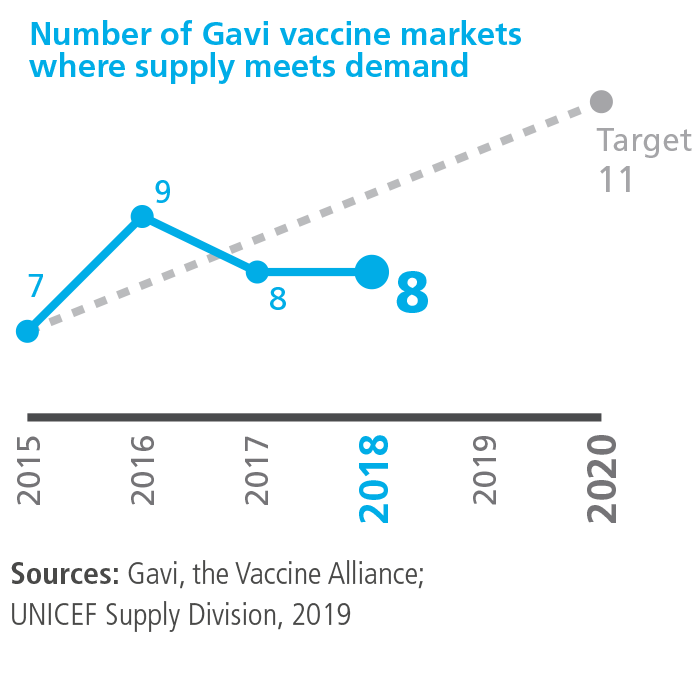

Sufficient and uninterrupted supply

What we measure

Number of Gavi vaccine markets where supply of appropriate vaccines is both sufficient and uninterrupted to meet demand.

2018 performance

By the end of the year, eight vaccine markets were reported to have sufficient and uninterrupted supply of appropriate vaccines – the same number as in 2017.

Markets meeting the definition of sufficient and uninterrupted supply were: Japanese encephalitis, measles, measles-rubella, meningitis A, oral cholera, pentavalent, pneumococcal and yellow fever. This is 73% of the 2020 target of 11 markets.

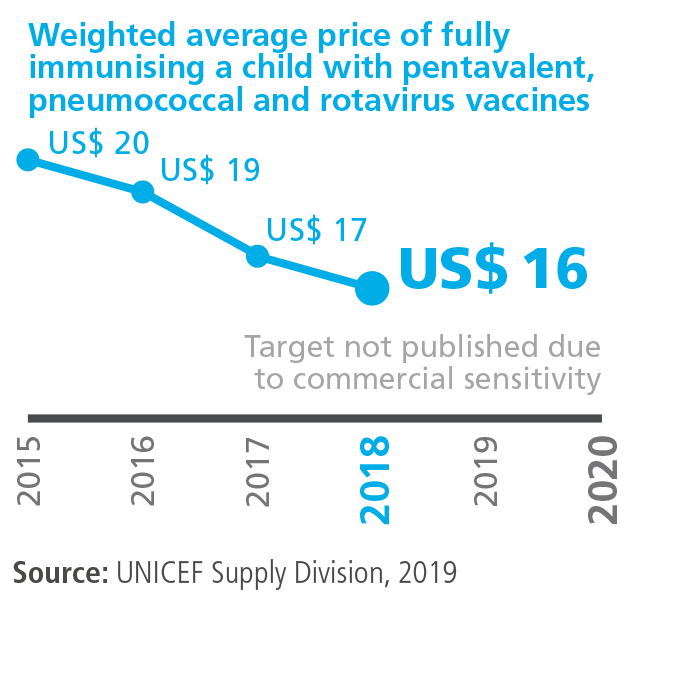

Cost of fully vaccinating a child with pentavalent, pneumococcal and rotavirus vaccines

What we measure

The weighted average vaccine price of fully immunising a child with pentavalent, pneumococcal and rotavirus vaccines.

2018 performance

By the end of 2018, the cost of immunising a child with a full course of pentavalent, pneumococcal and rotavirus vaccines averaged US$ 15.90. This represents a reduction of 21% relative to the 2015 baseline figure of US$ 20.01 and a 4% drop from the 2017 price of US$ 16.63.

The 2018 price reduction has been driven by recent falls in the cost of both pneumococcal and rotavirus vaccine. The price of one pneumococcal vaccine was reduced at the beginning of the year, thanks to a 2016 agreement, while the weighted average price of rotavirus vaccine fell by around 10% when a new supplier entered the market. The price of pentavalent vaccine has remained more or less stable following a substantial (43%) drop in 2017; this status quo has been achieved as a result of sustained effort on the part of Alliance partners to ensure that prices are sustainable for countries and manufacturers.

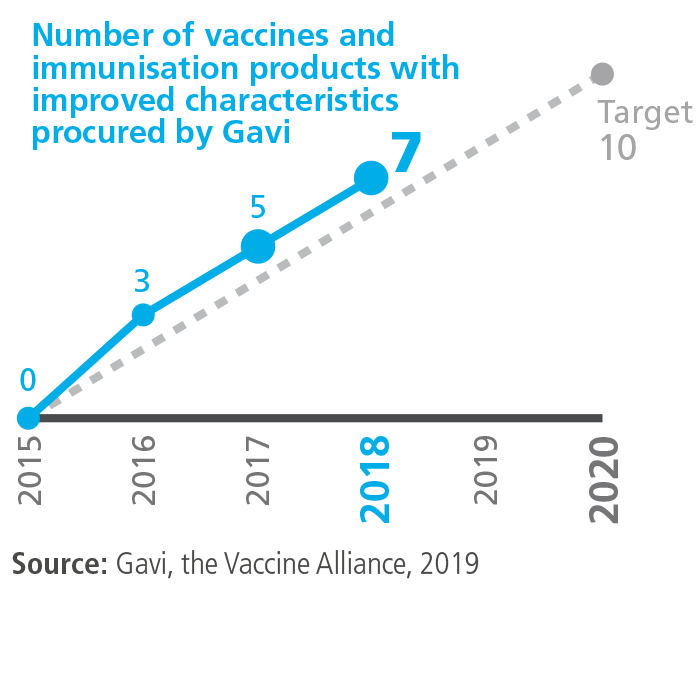

Innovation

What we measure

Number of vaccines and other related products with improved characteristics procured compared with the baseline year.

2018 performance

Since 2015, seven new products with improved characteristics that are WHO prequalified have been procured by Gavi, including two in 2018. Our 2020 target is a total of 10 new products.

The new products procured in 2018 comprised an oral cholera vaccine approved and labelled for controlled temperature chain use (allowing storage for up to 14 days at temperatures not exceeding 40°C) and a pneumococcal vaccine in a four-dose vial presentation.

Both of these products will help reduce pressure on countries’ cold chains. The cholera vaccine can be transported and stored for a limited period outside the traditional cold chain, as long as temperatures are controlled. The pneumococcal product offers volume-reduction benefits and as such will help to reduce cold chain capacity requirements.

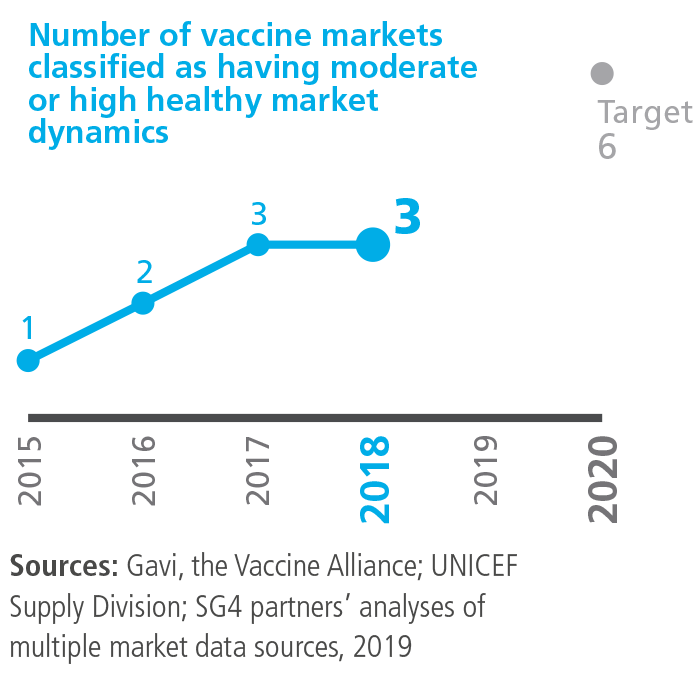

Healthy market dynamics

What we measure

Number of Gavi vaccine markets classified as benefiting from high or moderate health. Each vaccine market is rated as having high, moderate or low market health, or as having no healthy market dynamics.

2018 performance

Three vaccine markets were assessed as having moderate or high market dynamics in 2018, no change from 2017.

The market for pentavalent vaccine is mature and maintained its “moderate” market rating. As noted above, there was a substantial price drop in 2017, but careful and ongoing monitoring is needed to ensure long-term sustainability in the supply of this vaccine.

The yellow fever vaccine market also kept its “moderate” market rating. Increased levels of supply meant that demand for both routine immunisation and campaigns was met throughout the year, but as is the case in other markets, careful planning and monitoring are required to ensure that this balance is sustained.

While the pneumococcal vaccine market retained its “moderate” rating in 2018, there is a need to increase the number of suppliers if further improvements in the market dynamics for this vaccine are going to be achieved.

The remaining eight vaccine markets were classified as having “low” market health or inadequate supply.

Latest news

Gavi statement on scaling innovative financing for the next pandemic

As part of its Gavi Leap reforms, Gavi remains committed to working with countries and partners to accelerate and strengthen coordination on pandemic financing.

Gavi statement on the Ebola disease outbreak in Democratic Republic of the Congo and Uganda

Gavi, the Vaccine Alliance is closely monitoring the Ebola disease outbreak caused by Bundibugyo virus that is currently affecting the Democratic Republic of the Congo (DRC) and Uganda.